Thinkstock

Audio By Carbonatix

A new study estimates that it will take Denver millennials sixteen years to save enough to cover a down payment on a home. The reasons go beyond how difficult it is for young people to make a living in Denver despite the strong economy to include the failure of wages to keep up with housing costs, poor saving habits and misunderstandings about how much money it will take to purchase a house or condominium right now.

The data is drawn from “American Dream of Homeownership Delayed for Millennial Generation,” a report by ApartmentList.com. The results “underscore the long-term crisis that home ownership in the United States may face, as millennials delay buying a home until later in life,” write co-authors Andrew Woo and Chris Salviati. “One of the outstanding questions for the housing market has been whether or not the nation’s largest generation – millennials – will purchase homes at rates similar to their parents or if they will continue to rent long into adulthood, or even indefinitely.”

The analysis looks at these issues from a nationwide perspective, but in the following Q&A, conducted via e-mail, Woo provides Denver-centric facts and figures that show the Mile High City is among the toughest places in the country for millennials who want to move from renting to owning.

Here is plenty of information that millennials about to take a plunge into the red-hot real estate market absolutely need to know.

Westword: Your report looks at how the dream of home ownership has been delayed for many millennials. Would you say that millennials in Denver are typical representatives of this trend? Or is their situation actually more problematic than the one facing millennials in many other major cities?

Andrew Woo: Home ownership has been delayed for millennials nationwide, but the situation in Denver is particularly severe. Denver millennials will need sixteen years to save enough for a down payment. It will take Denver millennials around twice as long to save for a down payment as millennials in Orlando, Atlanta, Minneapolis and New York. Note that there are a few cities where the millennials will need even longer to save for a home than in Denver – specifically, San Jose (23.9), Austin (20.9), and Los Angeles (20.7).

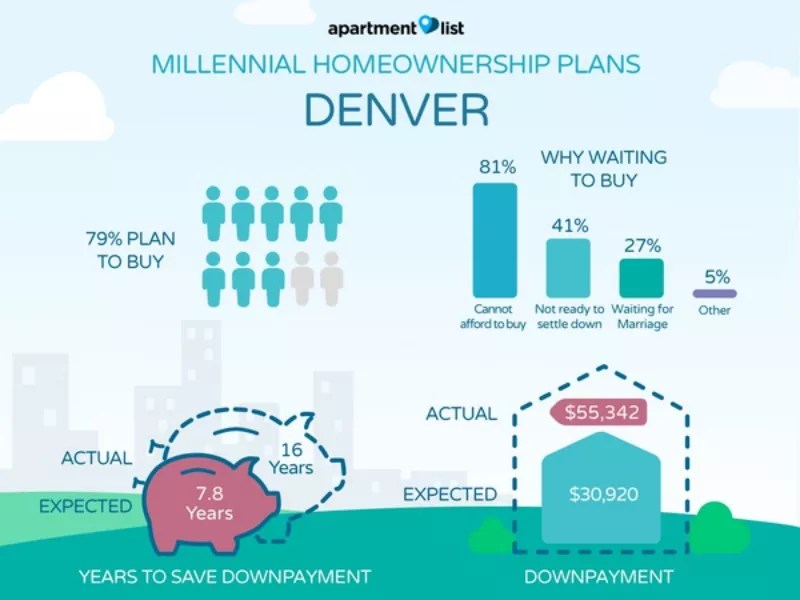

Your figures show that 79 percent of Denver millennials would like to purchase a home. Is this higher or lower than the national average currently – and how does it compare with people in this age group in the recent past?

Both nationwide and in Denver, the vast majority of millennial renters plan to purchase a home in the future. Nationwide, 80 percent of millennial renters would like to purchase a home compared to 79 percent in Denver. Nationally, the percentage of millennials planning to purchase a home in the future is slightly higher than in 2015 (79 percent) and 2014 (74 percent). In 2014, 9 percent of millennials said they expect to always rent, compared to just 5 percent in 2017.

This graphic shows how long it will take millennials in various major cities to save enough for a down payment on a home.

According to your data, 81 percent of Denver millennials who want to purchase a home feel that they can’t afford to do so. Is their reasoning sound, by and large? Or are a significant number of people in Denver holding off in part because they remember the bursting of the housing bubble a decade or so ago and fear the same thing happening to them, even if they have sufficient resources to make a purchase?

Only 4 percent of Denver millennials plan to purchase a home within the next year, and nearly a third plan to wait at least five years before purchasing a home. Affordability is the primary concern for 81 percent of Denver millennials. Currently, Denver millennials have saved around $5,000 for a down payment on average, which is not nearly enough to cover the average 20 percent condo down payment of $55,340. While some millennials may worry about another housing bubble, it seems that most simply don’t have enough saved for a down payment yet.

What are the biggest challenges facing Denver millennials who’d like to purchase a home?

Lack of down payment savings is the biggest challenge facing Denver millennials. The average down payment savings of $4,950 for Denver millennials is less than one-tenth of what is needed for a 20 percent condo down payment. Denver millennials are only setting aside $200 per month toward a down payment on average, so it will take them years to amass sufficient savings. Additionally, Denver millennials underestimate the amount they need to save for a down payment. On average, they expect to need $30,920 for a down payment, which is only 56 percent of the actual down payment of $55,340.

How do rising home prices in Denver factor in?

If home prices continue to rise, it could take Denver millennials even longer than sixteen years to save enough for a down payment. In our calculations, we have assumed that home prices will increase at the historical average growth rate over the past twenty years for the nation as a whole. If Denver home prices rise faster than this historical average, millennials will need longer to save for a down payment.

Denver’s economy is booming right now – but are wages failing to keep pace with housing costs? If so, why is there a lag?

Our analysis does not look at wage and housing cost growth at the metro level, but note that nationwide, wages are failing to keep up with rising rents and home prices. As the economy has recovered in recent years, an oversupply of labor (i.e. large numbers of unemployed and underemployed Americans looking for work) has allowed employers to delay wage increases; at the same time, an under-supply of new construction has exacerbated increases in housing costs. Stagnant wage growth coupled with high cost of living and expensive rents has made it harder for millennials to save for a down payment.

Are the main reasons that millennials are delaying the purchase of a home financial? Or are there other reasons that might contribute to an explanation?

Although financial concerns are the primary reason millennials cite for delaying homeownership, some millennials say they are waiting to buy a home because they are not ready to settle down or are waiting for marriage. In Denver, 81 percent of millennials cite affordability issues, while only 41 percent cite not being ready to settle down and 27 percent cite waiting for marriage.

Are there ways to purchase a home without a 20 percent down payment? If so, what are the potential risks and/or rewards?

Some lenders will offer lower down payments, but these loans often come with higher interest rates and mortgage insurance premiums. Millennials who pursue lower down payments will have higher monthly costs because of higher interest rates. Additionally, millennials with poor credit scores may not be able to pursue lower down payment options.

Why do Denver millennials underestimate the size of the down payment they’ll need to make?

Millennials in many cities underestimate the savings needed for a down payment. In Denver, millennials’ down payment expectation is only 56 percent of the actual price. Millennials expect to spend $30,920, while the actual down payment needed for a Denver condo is $55,340. Given that 58 percent of Denver millennials are not planning to purchase for at least three years, it seems likely that many of them have not begun researching actual down payments, which explains their unrealistic expectations and low savings rates. Additionally, Denver millennials may be anticipating purchasing with a down payment of less than 20 percent.

Another Apartment List graphic about millennials, housing and Denver.

By and large, do millennials in Denver and elsewhere save as much as they could? Or are they saving the maximum they can given their economic situation, and setting aside more would be impossible?

There are some indications that at least some millennials could be saving more for a down payment. Millennials with higher salaries save a smaller share of their income, indicating they could increase monthly savings. Millennials making $24,000 per year save around 10 percent of their income toward a down payment on average, while those earning over $72,000 save only 3.5 percent. Student loan debt, high rents and stagnating wages do provide additional challenges for millennials trying to save for home ownership.

If more and more people find the dream of home ownership impossible in Denver, does that portend a potential collapse of the local housing market? Or is there a less dire scenario?

While millennials may delay homeownership longer, the collapse of the Denver housing market seems unlikely. Some older and wealthier millennials are purchasing homes and will continue to do so. It’s also possible that millennials from more expensive markets such as Los Angeles, Boston and San Francisco will move to cities like Denver to be able to buy a home with a lower down payment. Additionally, there are signs that many developers across the country may increase construction of more affordable entry-level homes to meet increasing millennial demand, though it may be years before we fully see the effects of this.

Does this state of affairs seem likely to change anytime soon? If so, what needs to happen in order for more Denver millennials to move into home ownership?

While many Denver millennials will need well over a decade to save for a down payment, some millennials may start saving more each month in order to afford a home sooner. Programs to allow millennials to purchase homes with lower down payments could have a large impact on increasing millennial home ownership. Additionally, construction of less expensive condos and starter homes will help millennials in many cities, including Denver.

Do you have any other Denver-specific data that you can share and describe?

Although 79 percent of Denver millennials plan on purchasing a home, only 4 percent plan on doing so within the next year. Fifteen percent plan to purchase a home one and two years from now, 22 percent between two and three years from now, 27 percent between three and five years from now, and 31 percent in over four years.

Is there anything else on this topic that I may have neglected to ask but you feel is important to add?

While nearly 70 percent of Denver millennials plan to purchase a home within the next five years, with current savings, many will find themselves unable to afford a down payment.